Entry into monopolistically competitive industries is often introduced in a principles-level course with just a shift of the demand curve, however, the slope of the demand curve may be impacted by the availability of substitutes. This lesson outlines a lecture on the entry decision for firms entering monopolistically competitive industries by changing the slope of the demand curve. It highlights changes to consumer and producer surplus and equilibrium conditions. The lesson starts with the assumption of constant marginal cost, but allows for an extension with more traditional u-shaped cost curves. The description is consistent with both figures, allowing the instructor to determine the cost curves appropriate for their class.

Episode Title: Demand for Meth in the Czech Republic

Season: 5

Episode: 8

Episode Title: “Gliding Over All”

Timeframe: (08:47 — 11:22)

Concepts: comparative advantage, demand, elasticity of demand, elasticity of supply, expansion, exports, intra-firm trade, market entry, middleman, monopolistic competition, multinational enterprise, opportunity cost, product differentiation, trade barriers, transaction costs

Clip Summary

Lydia presents Walter with the opportunity of expanding into a new market (the Czech Republic). Lydia goes further and points out that entry should not be difficult given Walter’s high-purity “blue” methamphetamine and the inferior alternatives available there. Also, it is worth noting that such overseas expansion would not have been possible without Lydia’s expertise regarding global supply chains.

Lecture Summary

This outline assumes the market for crystal meth in the Czech Republic to be monopolistically competitive. It serves as a reference story to teach and discuss the effect of Walter’s decision on entering the market. The steps below cover market equilibrium, elasticity of demand, the Lerner Index, consumer and producer surplus, revenue, and deadweight loss.

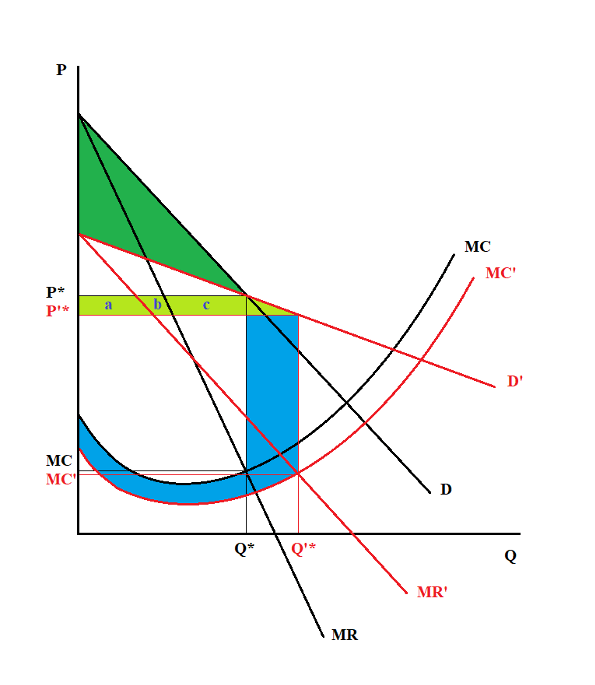

The initial market is drawn in black and emphasizes a market equilibrium at P* and Q*. The lines and notations in red denote the post-entry market outcome, under the assumption that Walter’s marginal cost of production is linear and similar to that of his competitors. The exercise can be conducted assuming Walter’s marginal cost of production is non-linear and lower/higher that that of his competitors. This situation is presented in Figure 2 at the end of the guide.

- Walter’s entry into the Czech market leads to a more elastic demand curve. Our initial demand curve (D) rotates to new demand curve (D’). When markets have more substitutes available, the elasticity of demand for any individual product is larger.

- With a flatter demand curve, the marginal revenue curve is not flatter as well. The original marginal revenue curve (MR) rotates to the new marginal revenue curve (MR’).

- Monopolistically competitive firms produce where the marginal revenue equals marginal cost. With the entry of Walter into the market, the equilibrium quantity increases from Q* to Q’*.

- With the increase in output, prices fall, but this can also be seen using the markup rule. An increase in elasticity will reduce the size of the markup. The equilibrium price decreases to from P* to P’*.

- Consumer surplus is the difference of people’s willingness to pay and the price actually paid. In our graph, consumer surplus is the area beneath the demand curve and above the equilibrium price. With the demand, equilibrium price, and equilibrium quantity shifts show on the graph above, consumer surplus decreases by the dark triangle, but increases by the light green area.

- Producer surplus is the difference between the equilibrium price and the marginal willingness to supply. The marginal willingness to supply a product is based on a firm’s marginal cost of production. For this scenario, producer surplus is the area beneath the equilibrium price and above the marginal cost curve, but only up to the equilibrium quantity. Producer surplus decreases by area (a + b +c) through the price effect, but gain the blue shaded area as part of the quantity effect.

Lecture Extension

While constant marginal costs may be appropriate in a principles level course or as a review in intermediate microeconomics, an instructor may wish to extend the conversation with a discussion of marginal costs with decreasing and increasing returns to scale. Figure 2 presents the same market entry decision as above, but replaces the constant marginal cost assumption with u-shaped cost curves:

Under this scenario, Walter’s entry into the larger market allows him to exploit economies of scale and lower his cost of production from MC to MC’. The profit maximization decisions mentioned above match the same outline/shading as the constant marginal cost story.